The 71-page study, analysing 269 villa projects and 56 condominium developments across the island, found that Phuket’s residential sector is benefiting from demand fundamentals that have strengthened well beyond pre-pandemic levels, with branded residences and compact, investment-grade units delivering standout results.

Phuket generated B497 billion in tourism revenue in 2024, the highest in a decade and a 28.2% increase year-on-year. Average tourist spending rose to B51,428 per trip, exceeding 2019 levels, with accommodation accounting for nearly half of visitor expenditure, up from 38% before the pandemic.

“The scale and quality of tourism demand we are seeing in Phuket is directly translating into residential demand,” said Phattarachai Taweewong, Director of Research Services at Colliers Thailand.

“This is being reinforced by continued interest from international buyers across Russian, Chinese, Middle Eastern, Indian and Western European markets.”

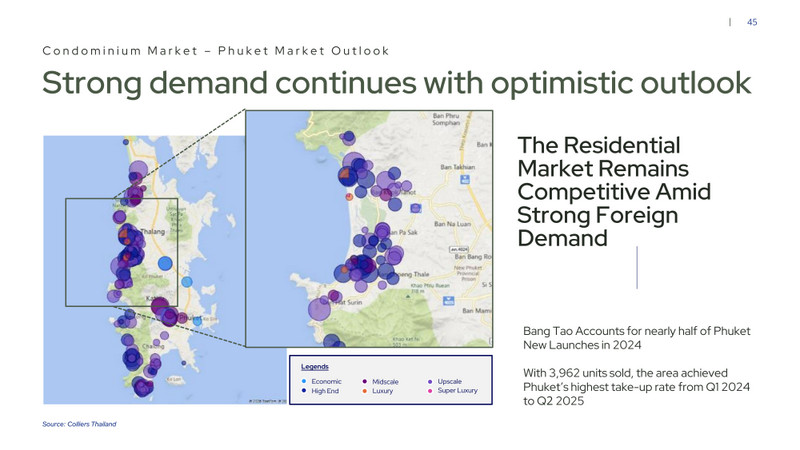

Bang Tao emerged as the island’s dominant residential hotspot, accounting for more than 40% of new condominium supply launched between Q1 2024 and Q2 2025. During the period, 7,993 of the 18,767 new condominium units introduced to the market were located in the Bang Tao area, positioning it as one of Southeast Asia’s most active luxury residential zones.

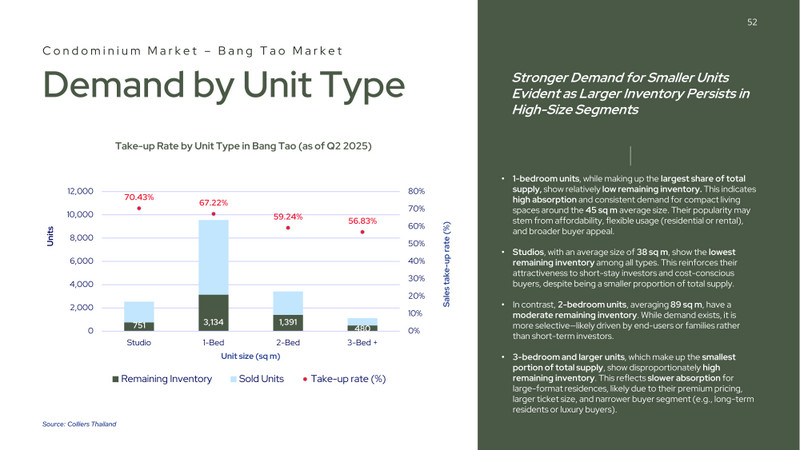

The research highlighted a clear market shift toward smaller, investment-grade units with strong resale and rental appeal. One-bedroom units sized between 31 and 50 square metres represented 57% of total supply, or 9,561 units, while recording the lowest levels of remaining inventory. Studio units demonstrated the fastest absorption across all segments.

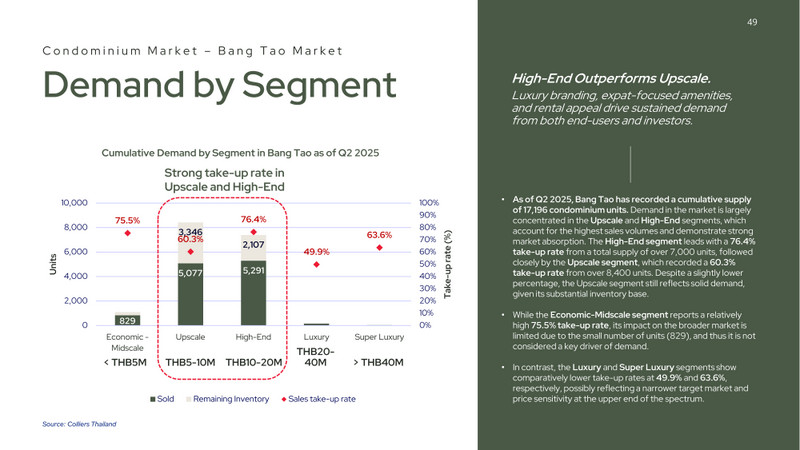

High-end condominiums priced between B10 million and B20mn achieved a take-up rate of 76.4%, indicating continued depth of demand despite a record volume of new supply entering the market in 2024.

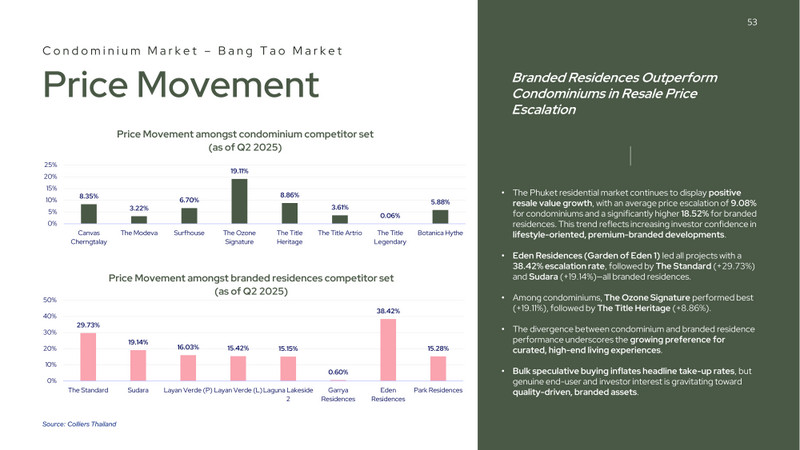

Branded residences were identified as the strongest-performing product category. Across the Q1 2024 to Q2 2025 period, branded projects recorded average price appreciation of 18.52%, more than double the 9.08% achieved by traditional condominiums. Top-performing branded developments delivered gains of up to 38%, while leading traditional projects achieved appreciation of up to 19%.

Low-density developments with fewer than five units per floor commanded price premiums of approximately 10-12%, with branded residences averaging B180,000 to B210,000 per square metre, compared with B140,000 to B176,000 per square metre for non-branded projects.

“What stands out is the sustainability of demand,” said AYANA Board Director Jimmy Yan. “Buyer composition, product quality and location are aligning in a way that supports long-term value creation rather than short-term speculative activity.”

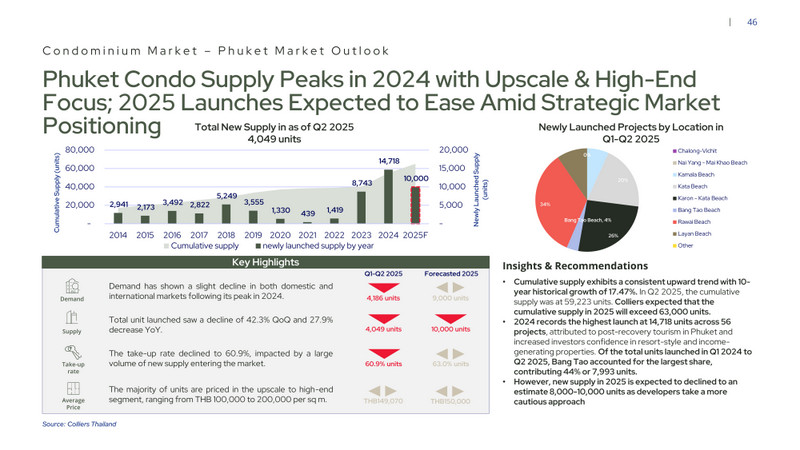

From a supply perspective, 2024 marked a peak year, with 14,718 condominium units and 1,942 villas launched, representing a combined project value of B124bn. The market is expected to moderate in 2025, with approximately 8,000 to 10,000 new condominium units forecast, while annual project values are expected to remain stable at B70-80bn.

The villa market continued to show resilience, with 4,903 units across 269 projects recorded as of Q2 2025. Total demand stood at 2,597 units, with the sub-B15mn segment showing the highest monthly absorption rate at 6.7%, followed by the B70-100m luxury segment.

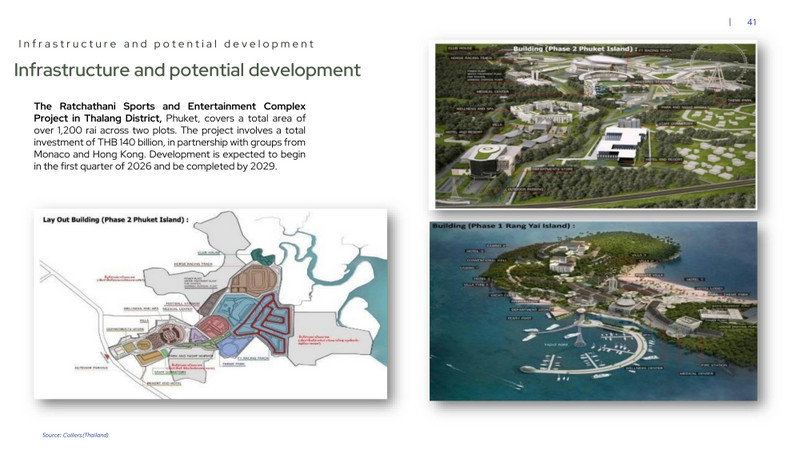

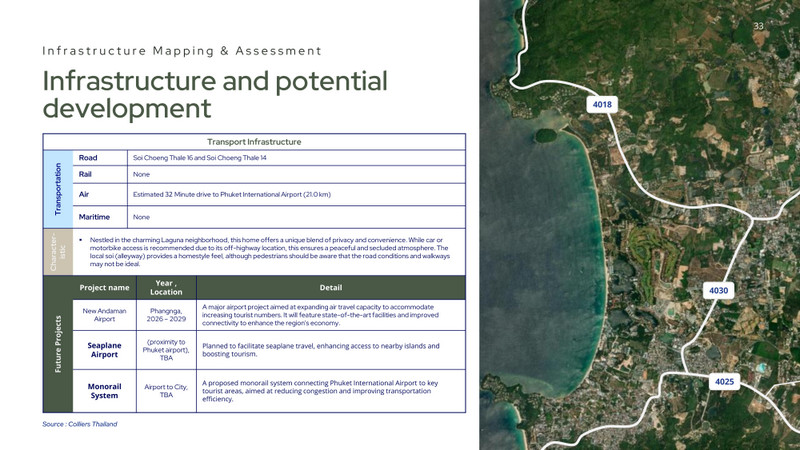

While demand fundamentals remain the primary driver of market performance, the report noted that Phuket’s long-term outlook is further supported by a B148bn infrastructure programme scheduled through to 2033.

Key projects include new expressway links, port upgrades, a major sports and entertainment complex and expansion of Phuket International Airport, all of which are expected to enhance accessibility and reinforce the island’s position as a regional luxury residential destination.

The research concludes that Phuket’s property market is transitioning into a more mature growth phase, led by tourism-driven demand, product differentiation and strong international buyer confidence.