However, escaping tax in Australia just got a lot harder. The Australian Government announced late last year that it would "modernise" the individual tax residency provisions in the 2021-22 Federal Budget to refocus on physical presence, Australian connections, and other objective criteria.

Not that the Australian Tax office (ATO) is noted for its leniency. The ATO issued guidance on how it will consider tax residency for the 2020- and 2021-income years considering COVID-19 and closed borders. Any tolerance dissolved once borders opened to travel again, no matter how inconvenient.

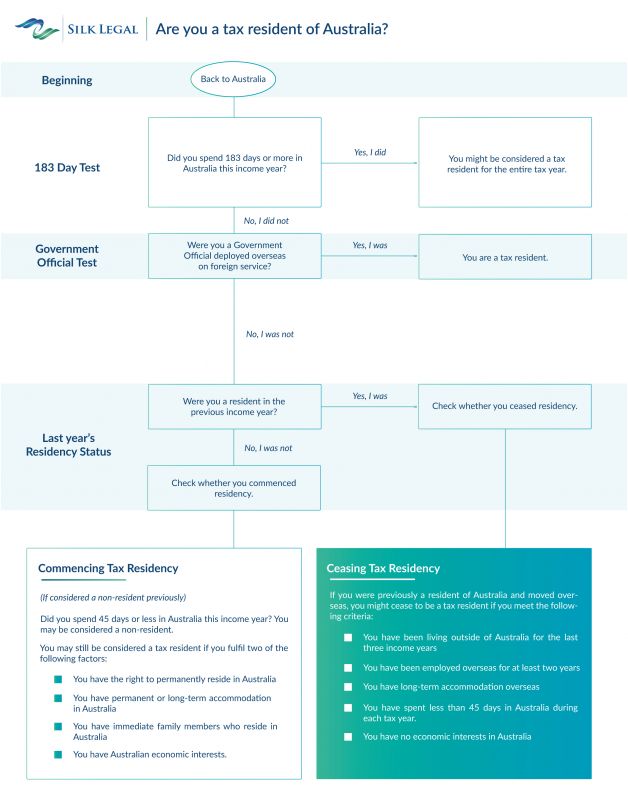

With this so-called “modernisation,” the Australian Government is planning to introduce a "bright line" test as the primary test for residency and tax. This means if an individual spends 183 days or more in Australia, they will automatically be considered a tax resident of Australia and taxed in Australia on your global income. There is no need for any further consideration on where the individual’s family members are, where their assets are situated, etc.

Currently, you are not considered a tax resident of Australia if you can show that you "usual[ly]" live outside Australia, even if you spend more than a total of 183 days in Australia in any one tax year.

But this isn’t the end to the changes.

Even if you spend less than a total of 183 days in Australia, the taxman can apply a secondary test to see if you should be taxed in Australia based upon:

- Whether you can reside permanently in Australia; and/or

- Whether you own or rent a house in Australia; and/or

- Whether you have family in Australia; and/or

- Other Australian economic interests. This includes any form of employment in Australia; actively participating in a business in Australia; significant Australian assets which include property, money in bank accounts or an interest in a family trust.

OOPS - BECOMING A TAX RESIDENT AGAIN

Even if you spend less than a total of 183 days in Australia during the tax year and were a foreign resident during the previous income year, you could be considered a tax resident of Australia again if you spend a total of more than 45 days in Australia during one tax year and satisfy two or more of the factors listed above.

The Government’s new proposal makes your tax status change a more gradual process and needs to be proven over a few years.

An example

Barry is Australian and moved to Thailand in 2019. With the COVID pandemic, he didn’t return to Australia from 2019 to 2021. In 2022, he plans to spend a few months with his children in Melbourne but has sold all his investments in 2020. Barry still considers himself to be a foreign resident for income since 2019 based on the current tax residency rules. In the 2022 tax year (after the changes to the legislation have been made), he spent 80 days in Australia visiting his family.

Barry will be considered a resident of Australia as he has spent more than 45 days in Australia during the tax year and satisfies two of the following factors:

- Barry is an Australian citizen, and has a right to reside in Australia; and

- His immediate family members are in Australia.

Barry’s investments are all taxable at Australian rates along with the money he is paid consulting to his old company.

THE BOTTOM LINE

Changing tax residency affects your income tax and capital gains tax (CGT) liabilities.

If you become an Australian tax resident, even by mistaking the new rules, you will probably be taxable on your worldwide income. For Capital Gains Tax purposes, you may have acquired assets that are not considered to be taxable Australian property (TAP) at market value. Non-TAP assets include real property situated overseas, foreign shares, etc.

If you bought your dream condo in Phuket, be careful. You may be deemed to have disposed of non-TAP assets at market value when they cease to be Australian residents. This may lead to an Australian CGT liability.

You can elect for this CGT event not to apply, but this means that the asset is "stuck" within the Australian tax net until sold or you regain your Australian tax residency status.

You need to do some tax planning if you sell your non-TAP assets at their market value on leaving Australia. In addition, you might not be entitled to any tax-free threshold, 50% CGT discount and the main residence exemption.

Similarly, if you have ownership of foreign companies, partnership or trusts (e.g., a Thai company holding property), this could impact the residency status of these foreign companies or trusts. For example, if you have set up a family discretionary trust this could be taxed as residents of Australia if any trustee is a resident in Australia at any time during an income year.

LEAVING THE TAXMAN BEHIND

If you convince the taxman you are a foreign resident, then generally you will only be taxed on your Australian income. Some of your Australian income may also be taxed at a concessional rate (e.g., interest earned in Australia is only subject to a 10% final withholding tax).

Generally, if you leave Australia then you need to spend less than 45 days in the current income year in Australia and less than a total of 45 days in Australia in each of the two preceding income years to be considered a foreign tax resident.

If you move offshore for employment, another rule called the “employment test” applies. To qualify as an offshore resident for taxation, you will need to be employed offshore for several years and prove that you:

- Resided in Australia for the 3 prior income years; and

- Have been employed overseas for more than 2 years; and

- Had a residence in the place of employment for the entire employment period; and

- You spent less than 45 days in Australia in each of the two preceding income years.

THE THAI-AUSTRALIA DOUBLE TAX AGREEMENT

Many Australians will now fall into the Australian tax net with the new lower 45-day threshold.

This may lead to situations of dual tax residency - where you are considered a tax resident of two countries. The provisions of the Thai-Australian Double Tax Agreement essentially treat you as a tax resident of only one country based on a “tie-breaker test”.

Be careful about what you wish for because if the taxman agrees, you are now a foreign resident, and under the new Australian proposals you will lose your entitlement to the tax-free threshold, 50% CGT discount, and main residence exemption. Furthermore, a CGT event and the additional tax may also apply depending on the final rules.

WHAT CAN I DO?

If you plan to come to Australia for extended holidays, you may want to think twice if you wish to still be treated as a foreign resident for Australian taxes in the future.

Australian expats should be aware that the proposed changes have not yet been legislated. Although it seems likely they will come into effect from 1 July 2022, you need to plan for this change and not be caught with an expensive tax bill.

By Dr Paul Crosio / Silk Legal

Paul Crosio is a Partner at Silk Legal & founding partner of Silk Advisory. He is a practicing Australian lawyer with over two decades of corporate experience in turn-around management in Thailand and abroad.